American Express analysis

A potential value opportunity during a time of heightened volatility.

Company Overview

American Express (AXP) is a leading global financial services company specializing in credit cards, charge cards, and payment processing. Operating a closed-loop payment network, AXP issues cards, processes transactions, and manages merchant relationships, differentiating itself from Visa and Mastercard. Its business can be seen in three main segments:

Global Consumer Services: Offers premium cards to affluent consumers, generating fees, interest, and merchant discounts.

Global Commercial Services: Provides corporate cards and expense solutions for businesses.

Global Merchant and Network Services: Handles transaction processing and merchant partnerships.

AXP’s premium brand and high-spending customer base drive strong margins. In 2024, AXP reported ~$65 billion in revenue, fueled by card fees and transaction growth, with a visible recovery in travel and dining.

Key Strengths:

Closed-loop model ensures pricing power and data insights. (Different from Visa and Mastercard which are open loop)

Loyal, affluent customer base with high per-card spending.

Diversified revenue (fees, interest, discounts).

Global expansion potential in under penetrated markets. Currently Amex lags behind competitors potentially pointing towards global growth

Key Risks:

Sensitivity to economic downturns affecting consumer spending.

Competition from fintechs (PayPal, Affirm).

Regulatory risks on fees and lending.

High rewards and marketing costs.

Financial Performance

Revenue: Grew from $36.1B (2020) to $65B (2024), 15% CAGR.

Net Income: Rose from $3.1B (2020) to $9B (2024).

Free Cash Flow: $5–7B annually, supporting dividends ($2.80/share) and buybacks ($8B in 2024).

Balance Sheet: $50B debt, $10B cash (net debt $40B).

Market Position:

Stock Price: $258.

Market Cap: $180.89B (701.11M shares).

P/E Ratio: 20x.

Dividend Yield: 1.1%.

Created with TradingView

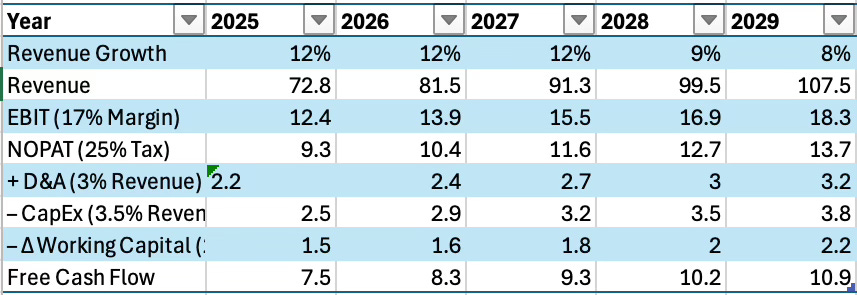

DCF MODEL:

Terminal Value (2029):

FCF2029: $10.9B.

Terminal Value = 11.28 / (7% – 3.5%) = $322.3B.

Sum of PVs: $267.2B.

Enterprise Value: $267.2B.

Equity Value: $267.2B – $40B = $227.2B.

Per-Share Value: $227.2B / 701.11M = $324.02.

Strategic Outlook

Growth Drivers:

Premium Cards: Platinum and Gold cards drive high-margin fee income

Digital Investments: Enhanced mobile apps and fraud detection.

Global Expansion: Growth in Asia and Europe increases transaction volume, an untapped market in comparison to competitors.

Corporate Services: Rising adoption of small business cards strengthens revenue.

Challenges:

Economic Sensitivity: Recessions could impact spending, though American Express’s wealth customers may mitigate this.

Fintech Competition: PayPal and Klarna challenge lending products.

Rewards Costs: High perks require careful cost management, an issue they have mastered thus far.

Industry Context:

The payments industry grows ~7–8% annually, supporting American Express’s trajectory.

The closed-loop model offers margin advantages but demands significant marketing spend in order to bring in new customers.